- The Wall Street Rollup

- Posts

- What you Need to Know for May 8th

What you Need to Know for May 8th

Guess which stocks fell 28% and 31% yesterday?

HY Harry

May 08, 2026

Together with Qualitate

Welcome back

The big news from last night is a federal trade court declared the 10% global tariffs President Trump imposed in February to be unlawful. Tariffs have definitely taken a back seat lately, but the administration is still working through more tariffs it may impose, giving the EU until July 4th to ratify its trade deal or face tariffs at much higher levels.

In Iran, the U.S. and Iran traded fire in the Strait of Hormuz, with President Trump calling the U.S. self-defense strikes “just a love tap”. Iran had launched multiple missiles and drones at U.S. ships passing toward the Gulf of Oman.

Today’s piece is sponsored by Qualitate, an AI-powered expert intelligence platform for finance professionals.

Let’s get into it.

Earnings Corner 💸

Disney $DIS ( ▲ 2.87% ) Revenue beat at $25.2B vs. $24.8B and EPS beat at $1.57 vs. $1.49, riven by continued strength in streaming and parks. Streaming revenue rose 13% as Disney+ and Hulu benefited from higher pricing, engagement, and advertising demand, while higher guest spending and cruise growth helped offset softer international tourism and a slight decline in U.S. park attendance. Disney reaffirmed its earnings growth outlook and increased its buyback plan.

Uber $UBER ( ▲ 3.36% ) revenue slightly missed at $13.2B vs. $13.29B but EPS beat at $0.72 vs. $0.71 and gross bookings were up 25%y/y. Growth was driven by strong trip volume (+20%), resilient mobility and delivery demand, and continued Uber One/premium momentum (now surpassing 50M users), while profitability also benefited from operating leverage and insurance cost savings. The company guided 2Q bookings above expectations, signaling demand remains strong.

DoorDash $DASH ( ▲ 2.89% ) revenue missed at $4.04B vs. $4.15B, but EPS beat at $0.42 vs. $0.37 as total orders jumped 27% y/y to a record 933M and GOV rose 37% to $31.6B. Growth was driven by strong consumer demand, record monthly active users and DashPass engagement, while management said the revenue miss was partly impacted by winter storms and Deliveroo integration timing. The company also guided 2Q GOV above expectations.

ARM Holdings $ARM ( ▲ 4.41% ) Top and bottom line beat with revenue of $1.49B (+20% y/y), driven by strong AI and data center demand as cloud royalties more than doubled y/y and Arm expanded CPU adoption across hyperscalers. However, weaker smartphone demand and memory shortages pressured mobile royalties, while supply constraints raised concerns about fully meeting $2B+ of demand for its new AI-focused data center CPUs.

Novo Nordisk $NVO ( ▲ 3.23% ) revenue beat with sales up 24% y/y while EPS missed. Strong demand for Wegovy and Ozempic, especially the new Wegovy pill launch in the U.S., supported growth, while pricing pressure and higher costs weighed on profitability. The company slightly raised guidance on continued GLP-1 demand.

McDonalds $MCD ( ▲ 0.83% ) Top and bottom line beat with revenue at $6.52B, as value meals, higher guest spending, and menu launches like the Big Arch burger supported traffic in a tougher consumer environment. Global same store sales rose 3.8%, though management warned higher gas and beef costs are continuing to pressure low income consumers.

Marriott $MAR ( ▼ 0.45% ) driven by higher room rates, resilient international travel demand, and continued hotel expansion with a record pipeline of 4,100+ properties, despite a softer macro backdrop. The company guided weaker near-term results as slowing U.S. travel demand and macro uncertainty are expected to pressure growth.

Airbnb $ABNB ( ▼ 0.56% ) revenue beat at $2.68B while EPS slightly missed, as strong global travel demand, higher pricing, and product updates like “Reserve Now, Pay Later” drove bookings and gross booking value growth. International expansion and new users remained strong, though Middle East conflict-related cancellations pressured nights booked growth.

DraftKings $DKNG ( ▲ 1.88% ) ervenue beat at $1.65B vs. $1.64B while EPS slightly missed, as strong customer engagement and higher sportsbook margins drove growth. Profitability improved as sportsbook revenue rose 24% and average revenue per user jumped 21%, though guidance was below expectations.

Cloudflare $NET ( ▼ 2.91% ) revenue beat at $640M vs. $622M and EPS beat. Demand continued accelerating and enterprise adoption remained strong, but the company announced layoffs impacting 20% of staff as it restructures around an “AI-first” operating model after internal AI usage surged.

On The Move 📈 📉

Shake Shack $SHAK ( ▼ 5.5% ) stock plunged after the company missed Q1 2026 revenue and earnings expectations, reported a $2.6M operating loss, and fell to a 52-week low.

Datadog $DDOG ( ▼ 19.03% ) jumped after beating revenue and earnings expectations and lifting its guidance for the year, with AI driving strong demand for cloud infrastructure.

Planet Fitness $PLNT ( ▼ 9.51% ) fell hard after lowering guidance and cancelling planned price hikes due to slower member growth.

The Trade Desk $TTD ( ▼ 6.8% ) fell -15% after hours after posting weak guidance, lower than expected profitability, and after losing a key executive to OpenAI.

Krispy Kreme $DNUT ( ▲ 4.19% ) reported in line earnings, is planning to open at least 100 new stores this year, and now expects net leverage <5.5x.

IPO Roundup 📍

Surveillance firm Hawkeye 360 $HAWK ( ▲ 5.02% ) gained 31% on its first day of trading after raising $416mm in its U.S. IPO, giving the company a market value of $3.2B.

Cerebras and lead bank Morgan Stanley are requiring limit orders from institutional investors as demand for its IPO continues to grow. Cerebras is seeking to raise $3.5B in the offering, which prices May 13th.

For deeper, stock market research upgrade to the WSR Investing Club

24 client interviews. Under 4 days. One-sixth the cost of a traditional expert network

That's how a top PE firm diligenced a fast-growing developer tools deal on Qualitate.

Qualitate's AI-powered platform runs the full sprint: question design, expert sourcing, structured voice interviews, and a finalized briefing report.

Trusted by 6 of the top 15 PE firms, leading hedge funds, and credit teams.

Today’s Headlines 📖🍿

Hantavirus latest: Health authorities are monitoring the Americans who recently returned from the MV Hondius, the cruise ship at the center of the outbreak that caused three deaths and left several others sick. While serious precautions are being taken, the WHO has stated that the hantavirus is less transmissible than Covid or the flu.

Claude for Microsoft 365 is here: Anthropic announced that Claude for Excel, PowerPoint, and Word are now generally available, while Claude for Outlook is in public beta. The AI can carry context across Microsoft apps, and appears to be a major upgrade over the Copilot add-ins many professionals currently use.

Banks face losses on hung Qualtrics deal: A JPMorgan-led group is set to absorb ~$500M on $5.3B of acquisition financing after failing to syndicate the debt, underscoring investor resistance to software exposure and tighter lending standards.

BlackRock credit fund hit by renewed markdowns: The firm cut NAV ~5% at its publicly traded BDC after $35M in losses, following a prior 19% write-down, as software-heavy exposure continues to drag and scrutiny builds across private credit valuations.

Meanwhile, a $10B Golub fund capped withdrawals at 5% after investors sought to pull 8.5% of shares.

Private equity talent shifts amid carry compression: Hunter Point Capital is seeing rising inflows of senior resumes from larger firms. A decline in carried interest is reshaping compensation and driving "a realignment of the entire talent landscape".

Blue Owl may move into credit secondaries: The firm is launching its first fund to buy secondhand private credit, positioning to deploy capital into discounted stakes.

Drake-backed Venezia FC raises €100M: New capital led by Tim Leiweke comes in ahead of top-tier competition, underscoring a continued institutional push into European football as an investable asset class.

AI token costs are rising: A JPMorgan report highlighted how several internet companies, including $META ( ▲ 0.19% ) , $SPOT ( ▼ 1.49% ) , $SHOP ( ▲ 2.22% ) , and $PINS ( ▼ 0.13% ) , have flagged cost headwinds due to higher spending on cloud, compute, and GPU capacity. The report warned that this could significantly shrink profits unless companies can accelerate revenue or find other cost savings.

Ramp eyes $40B: The corporate card startup is eyeing a $750mm fundraise co-led by Iconiq Capital and GIC at a $40B+ valuation, up from $32B in late 2025.

M&A Transactions💭

Sony is finalizing a deal to acquire a music catalog from Blackstone for nearly $4.0B. The catalog includes works of Justin Bieber and Neil Young.

Grand Bahama Power Company, provider of electricity services, was acquired for $280.0M by Bahamian Government.

Dr. Mohammed bin Rashed Al-Faqih & Partners, provider of medical services, has reached a definitive agreement to be acquired for SAR 1.596B by Fakeeh Care (SAU: 4017). EV/EBITDA was 14.23x and EV/Revenue was 3.42x.

Autronica Fire and Security, manufacturer of fire and gas detection and prevention equipment, has reached a definitive agreement to be acquired for $555.0M by MSA Safety (NYS: MSA). EV/Revenue was 3.47x.

Perfuse Therapeutics, operator of a biotechnology company, has reached a definitive agreement to be acquired for $2.45B by Bayer (ETR: BAYN). Centerview Partners advised on the sale.

Peakstone Realty Trust, a real estate investment trust, was acquired for $1.85B by Brookfield Asset Management. EV/Revenue was 14.05x. Bank of America advised on the sale.

Indicor, manufacturer of diversified industrial products, has reached a definitive agreement to be acquired for $5.0B by AMETEK (NYS: AME). EV/Revenue was 4.55x.

Cross Country Healthcare (NAS: CCRN), a healthcare workforce solution, has entered into a definitive agreement to be acquired for $437.0M by Knox Lane. EV/Revenue was 0.41x. Bank of America advised on the sale.

An undisclosed investor has reached a definitive agreement to acquire The Canadian Commercial Fields Business Unit of Cenovus Energy (TSE: CVE) for CAD 275.0M. TD Security advised on the sale.

Brazos Midstream, operator of a natural gas and crude oil company, has reached a definitive agreement to be acquired for $1.6B by Western Midstream Partners (NYS: WES). As part of the transaction Western Midstream Partners will pay approximately $800.0M in cash and issue approximately $800.0M in Western Midstream Partners common units at closing. EV/Revenue was 66.12x. Jefferies advised on the sale.

Reap, developer of a digital payment platform, has reached a definitive agreement to be acquired for $600.0M by Kraken. Goldman Sachs and Cross River Bank advised on the sale.

PathAI, operator of a pathology platform, has reached a definitive agreement to be acquired for $750.0M by Roche.

Catalyst Pharmaceuticals (NAS: CPRX), a commercial stage, patient-centric biopharmaceutical company, has reached a definitive agreement to be acquired for $4.103B by Angelili Pharma. EV/EBITDA was 13.83x and EV/Revenue was 6.97x. J.P. Morgan advised on the sale.

The Commercial Business Division in India of FMC has entered into a definitive agreement to be acquired for $252.0M by Crystal Crop Protection. Bank of America advised on the sale.

Private Placement Transactions💭

XBOW, developer of an AI-powered autonomous penetration testing platform, raised $120.91M of Series C venture funding led by Samsung Venture Investment, DFJ Growth, and Northzone Ventures at a pre-money valuation of $879.1M.

Corgi, developer of an AI-powered insurance platform, raised $160.0M of Series B venture funding led by TCV at a pre-money valuation of $1.14B.

CellCentric, operator of a clinical-stage cancer therapy biotechnology company, raised $220.0M of venture funding from Sofinnova Partners and undisclosed investors.

Astranis, manufacturer of small satellites, raised $455.0M of venture funding through a combination of debt and equity. $300.0M of Series E venture funding was led by Snowpoint Ventures and Franklin Templeton Investments United Kingdom. The transaction was supported by $155.0M of debt financing.

Quantum Motion, developer of a scalable quantum computing architecture, raised $160.0M of Series C venture funding in a deal led by DVC and Kembara Fund.

Infinigence, developer of an AI infrastructure platform, raised over CNY 700.0M of venture funding led by Grand Mount Capital and Hangzhou Hi-Tech Financial Investment Group.

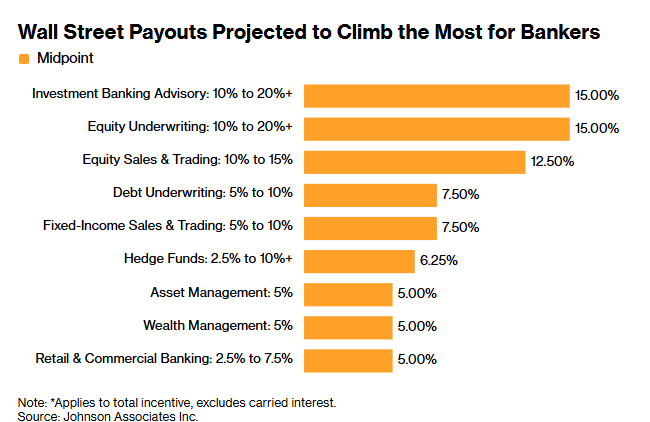

Noteworthy Chart 🧭

Looking for more comp data? Join Buyside Hub today to access a massive pool of wall street comp data.

Housekeeping Items:

Our Weekly Poll:

How are we doing?Tell us how we're doing and any feedback you have |

Upgrade to the WSR Investing Club: Receive high-conviction stock research & analysis to help you cut through the noise.

Recruit for Investment Banking: High Yield Harry and a group of Investment Bankers put together a 248 page deck for those recruiting for Investment Banking - sign up for free here to learn more about our decks.

Join beehiiv: Looking to start your own newsletter? Join beehiiv through us and you’ll get 30 days free and 3 months of a 20% discount.

Join our Referral Program and Gain WSR Investing Club Access ☕️

Enjoyed the newsletter? Send it to a friend 🤝

Obviously, none of this constitutes financial or investment advice. *Today’s Odds of the Day is in paid partnership with Polymarket