- The Wall Street Rollup

- Posts

- What you Need to Know for April 24th

What you Need to Know for April 24th

Citadel plays Chicken. ServiceNow leads the latest round of software turmoil.

HY Harry

April 24, 2026

Welcome back! Hope any NFL fans are happy with their team’s first round pick.

President Trump announced that Israel and Lebanon have agreed to extend their ceasefire by 3 weeks. Following the rapid market rally we’ve seen the past few weeks, investors took a bit of a breather yesterday to see if a more substantive path towards peace is on the cards.

Plus, ServiceNow’s weak results continued to shake the fragile Software industry further. More on that below. Let’s get into it.

Here’s a look at the earnings dropping today:

Friday: Procter & Gamble, HCA Healthcare, Colgate, Charter, Nomura, Moog, Oppenheimer

Here’s a look at economic data set to be released this morning:

Friday: April Consumer sentiment (49)

Earnings Corner 💸

Tesla $TSLA ( ▼ 14.19% ) missed on revenue ($22.39B vs. $22.64B) but beat on EPS ($0.41 vs. $0.37). Profit strength was driven by improved auto margins (higher pricing & lower material costs) and some one-time benefits tied to tariffs and warranty-related items, even as the core auto business remains under pressure from weaker demand. The company sharply increased spending with capex raised to $25B as it accelerates investment in AI, robotaxis, and robotics.

ServiceNow $NOW ( ▼ 1.68% ) had a terrible quarter with results only narrowly beating on revenue and EPS. The bigger issue was weaker subscription momentum, as delayed large deals in the Middle East (tied to geopolitical tensions) weighed on bookings, raising concerns about demand across the software sector.

GE Vernova $GEV ( ▲ 4.45% ) top and bottom line beat with revenue at $9.3B (+16% y/y) as surging demand from AI data centers drove a massive spike in power and electrification orders (+71%), EPS was boosted by non-recurring items. Upfront payments tied to that order strength fueled record free cash flow of $4.8B, and the company raised guidance as hyperscalers ramp infrastructure spend.

Boeing $BA ( ▼ 0.86% ) beat on revenue at $22.2B and posted a better then expected loss on EPS as higher aircraft deliveries (+10% y/y) drove improvement across commercial, defense, and services. Production is ramping on the 737 with backlog near record levels supporting the recovery, though free cash flow is still negative as the company continues spending to scale production and stabilize operations.

Southwest Airlines $LUV ( ▼ 4.57% ) missed on both revenue and EPS despite sales rising 13% y/y, as strong demand and higher fares (unit revenue +11%) were offset by higher fuel costs. 2Q EPS was guided below expectations due to rising fuel prices, full year outlook was held off because of cost uncertainty.

American Airlines $AAL ( ▼ 8.42% ) beat on both revenue and EPS as sales rose 11% y/y on strong demand, but higher fuel costs pressured profitability. The company sharply cut its full year guidance as fuel prices surge, even as premium and loyalty demand remain resilient

Intel $INTC ( ▼ 2.86% ) beat on revenue ($13.6B vs. $12.36B) and EPS ($0.29 vs. $0.01), with growth driven by surging AI demand in its data center segment and stronger PC demand, while margins also came in well above guidance (41% vs. 34.5%), signaling improving profitability. Guidance was well above expectations reinforcing that AI-driven demand is accelerating.

On The Move 📈 📉

Lululemon $LULU ( ▼ 1.99% ) stock fell after the company tapped a former Nike executive as its next CEO, with investors questioning whether this is the right hire to turn things around.

Netflix $NFLX ( ▲ 0.95% ) plans to buy back an additional $25B in shares after its failed Warner Bros bid, sending shares down slightly.

Texas Instruments $TXN ( ▼ 4.63% ) jumped after a strong forecast due to high demand for its analog chips, which are essential for data center buildout.

IBM $IBM ( ▼ 0.37% ) slid after failing to raise guidance for 2026.

For deeper, stock market research upgrade to the WSR Investing Club

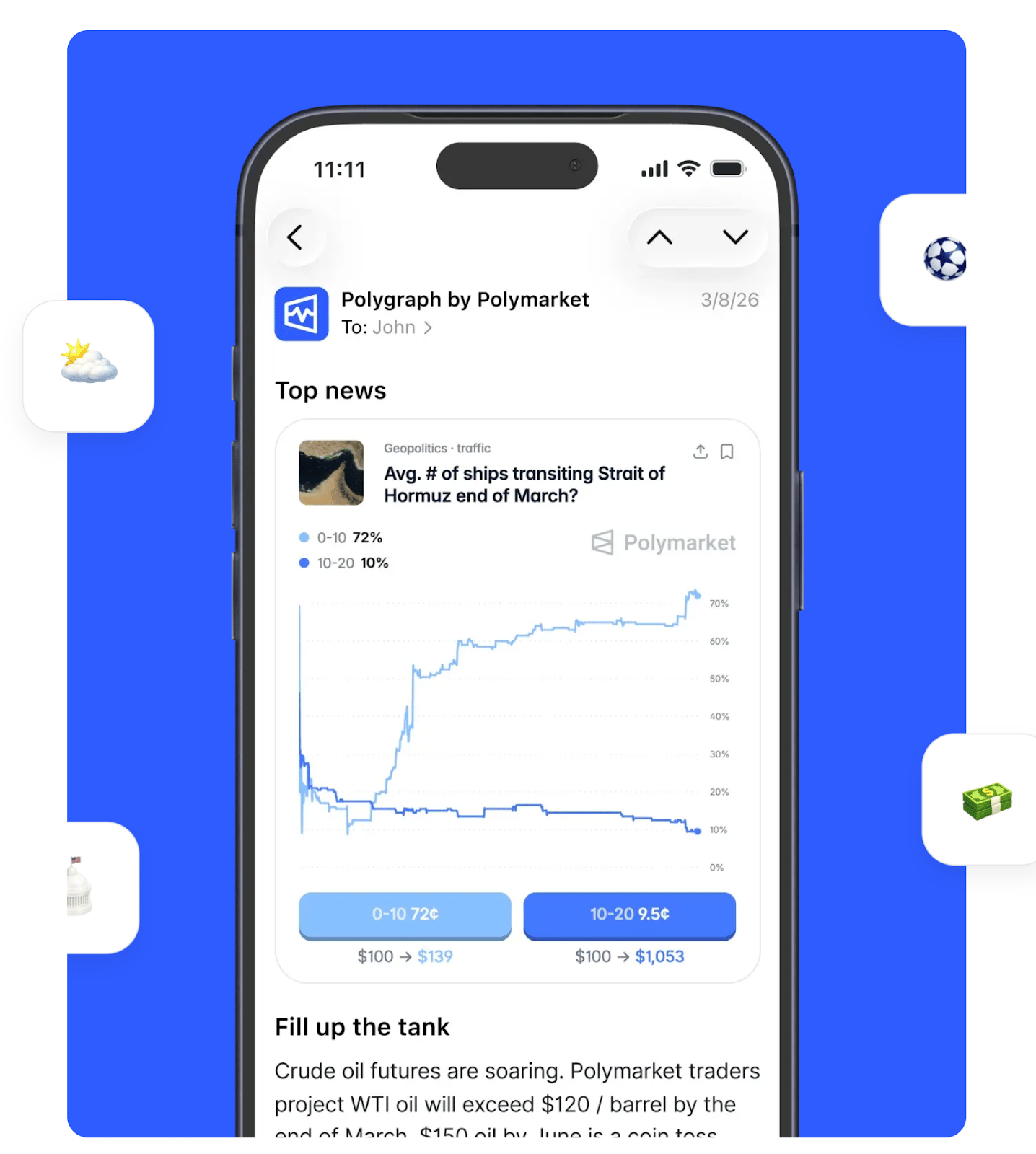

“I get my news on Polymarket”

Polygraph is news with skin in the game from the world’s largest prediction market.

Each morning, get an email breaking down everything happening on Polymarket: the biggest shifts in odds, breaking news, new markets, whale moves, and much more.

Join 1,428,136 readers who get their news on Polymarket.

Today’s Headlines 📖🍿

Citadel threatens to halt $6B NYC expansion amid tax fight: Ken Griffin’s hedge fund warned it would scrap its 350 Park Ave. redevelopment after Mayor Zohran Mamdani spotlighted Griffin’s $238M penthouse purchase to promote a new tax on $5M+ second homes, escalating tensions between City Hall and Wall Street.

Warner Bros. Discovery approved a $110B takeover by Paramount: Investors backed Paramount Skydance’s acquisition of WBD following a bidding war with Netflix and Comcast, clearing a key hurdle toward a Q3 close, while overwhelmingly rejecting CEO David Zaslav’s $800M+ golden parachute in a non-binding vote.

Thoma Bravo set to hand Medallia to lenders in $5.1B equity wipeout: The private equity firm is nearing a deal to cede control of the $6.4B software buyout to creditors, including Blackstone, KKR, and Apollo. This is one of the largest PE wipeouts in recent memory and is before material AI disruption.

AI infrastructure bets have emerged as a major winner for Blackstone, with President Jon Gray saying “it’s clearly the biggest driver for us today” as demand for compute power continues to soar. The firm was an early investor in the sector and now has over $150B in data centers globally, making it the world’s “largest investor in AI-related infrastructure.”

Junk investors are pushing for stronger protections: Sealed Air, Golden Goose, and TDC Brands have all tightened docs to get their deals done. High-yield spreads widened sharply in March as demand weakened, leading to investors negotiating for more borrower-friendly terms.

Air France-KLM, Lufthansa Advance in TAP Privatization Race: Portugal invited both carriers to submit binding bids for up to a 49.9% stake in TAP, setting up a showdown over the state-owned airline prized for its Brazil and transatlantic routes, with a final decision expected by early fall.

JPMorgan is set for a private credit push: The firm is committing to a strategy that will plow tens of billions into loans sourced by its own commercial bankers, aiming to narrow the gap with its rivals in the asset class. The firm is currently in talks to raise several billion dollars for the strategy.

Ingenico starts debt talks with creditors: The Apollo-backed payment terminal company has begun discussions with lenders over its "increasingly untenable" leverage. PIMCO is among the lenders being advised by Gibson Dunn and Houlihan Lokey.

The White House is nearing a rescue deal for Spirit Airlines, potentially loaning the carrier up to $500mm for warrants to take a significant stake in the company, possibly as high as 90%.

Corporate Layoffs:

Meta is cutting 10% of its workforce, aiming to boost efficiency and offset its heavy spending on AI. The layoffs will affect 8k employees, and the company also won’t hire workers for 6k open roles that it had planned to fill.

KPMG is laying off 10% of its U.S. audit partners after a voluntary retirement push fell short. The cuts aim to better align the number of partners with the size of the audit business.

Microsoft has announced a voluntary retirement effort of its own, with about 7% of U.S. employees eligible for the program. The company had several rounds of layoffs last year, and is looking to further shrink its workforce amid heavy spending on data centers.

M&A Transactions💭

MGM Northfield Park was acquired by $546.0M by Clairvest Group. The transaction was supported by an estimated $381.0M of debt financing. Jefferies and SMBC Nikko Securities advised on the sale.

LivePerson (NAS: LPSN), the enterprise leader in digital customer conversation, has reached a definitive agreement to be acquired for $434.784M by SoundHound AI (NAS: SOUN). EV/Revenue was 1.78x. Houlihan Lokey and Lazard advised on the sale.

Quintillion, provider of middle-mile backhaul services, has reached a definitive agreement to be acquired for $310.0M by GCI Communication. Bank Street Group advised on the sale.

Kashiv BioSciences, provider of pharmaceutical research and drug delivery services, has reached a definitive agreement to be acquired for $750.0M by Amneal Pharmaceuticals (NAS: AMRX). J.P. Morgan advised on the sale.

emuLab., provider of creative design and photography support services, has reached a definitive agreement to be acquired for $260.0M by Decorte Holdings (TKS: 7372).

Diamond Hill Capital Management, derives its consolidated revenues and net income from investment advisory and fund administration services, was acquired for $479.5M by First Eagle Investments. EV/EBITDA was 7.19x and EV/Revenue was 3.26x. Broadhaven Capital Partners advised on the sale.

Committed Advisors, provider of independent global private investment management services, was acquired for EUR 386.0M by Wendel Group (PAR: MF). The company will receive a contingent payout of EUR 128.0M upon the completion of FRE and fundraising targets. Rothschild & Co advised on the sale.

Celerion, provider of early-phase clinical research and bioanalytical testing services, has reached a definitive agreement to be acquired for $1.8B by Thomas H. Lee Partners. EV/EBITDA was 12.0x. Bank of America and Lazard advised on the sale.

SFR, a French telecom, has entered into a definitive agreement to be acquired for EUR 20.35BB by Bouygues Telecom (PAR: BOUY), Iliad-Free, and Orange (PAR: ORAN).

Kelonia Therapeutics, a clinical-stage biotech company, has entered into a definitive agreement to be acquired by Eli Lilly (NAS: LLY) for up to $7.0B, including a $3.25B upfront payout.

North Pacific Paper Company, manufacturer of paper packaging materials, has reached a definitive agreement to be acquired for $360.0M by International Paper (NYS: IP).

Neurona Therapeutics, developer of regenerative cell therapies, has reached a definitive agreement to be acquired for $1.15B by UCB (BRU: UCB). Centerview Partners advised on the sale.

Uranium Royalty Corp. (NAS: UROY) agreed to acquire 92% interest in Sweetwater Royalties, a uranium and critical minerals royalty platform, for an estimated $1.9B.

Metro Supply Chain Group, provider of third-party logistics services, La Caisse reached a definitive agreement to sell its 44% stake in the company to LDC Logistics Development for CAD 2.2B. The company will receive a contingent payout of CAD 400.0M upon the completion of future performance terms. J.P. Morgan advised on the sale.

Private Placement Transactions💭

Aria Networks, developer of an AI-focused networking platform, raised $100.0M of Series A venture funding led by Sutter Hill Ventures.

EVAS Intelligence, developer of AI computing chips, raised CNY 1.5B of Series B venture funding led by Beijing Economic-Technological Development Area Industrial Upgrading Fund, Beijing High-Precision and Cutting-Edge Industry Development Investment Fund, Beijing Information Industry Development Investment Fund, and Beijing Artificial Intelligence Industry Investment Fund.

Omni Analytics, developer of an AI analytics platform, raised $120.0M of Series C venture funding led by ICONIQ Growth at a pre-money valuation $1.39B.

Black Lake Technologies, developer of cloud-based technology for data-driven smart factories, raised CNY 1.0B of Series D venture funding from undisclosed investors.

Factory, AI coding company, raised $150.0M of Series C venture funding led by Khosla Ventures at a pre-money valuation of $1.5B.

Plata, a Mexican digital bank, raised $405.0M of Series C venture funding led by Bicycle Capital at a pre-money valuation of $5.0B.

Blue Energy, develop of prefabricated nuclear power plants, raised $380.0M of funding led by VXI Capital.

Zum, student mobility platform, raised $100.0M in funding from TPG Rise Fund at a pre-money valuation of $1.7B.

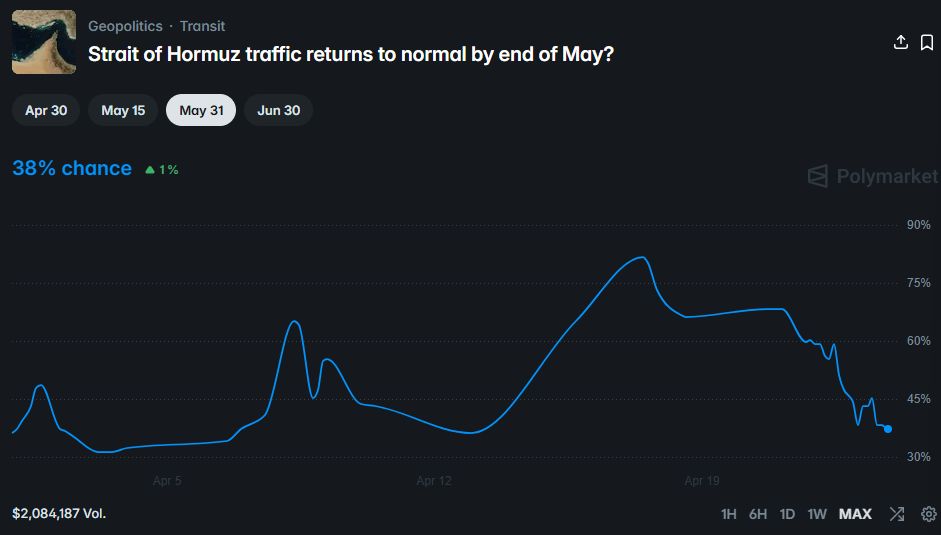

Chart of the Day

Odds of the Day 🍒

Polymarket traders are pricing in a 38% chance of Strait of Hormuz traffic being normal by the end of May

Housekeeping Items:

Our Weekly Poll:

How are we doing?Tell us how we're doing and any feedback you have |

Finance Jobs: Looking for a job in Finance? Join Buyside Hub to access the Job Board for free.

Upgrade to the WSR Investing Club: Receive high-conviction stock research & analysis to help you cut through the noise.

Recruit for Investment Banking: High Yield Harry and a group of Investment Bankers put together a 248 page deck for those recruiting for Investment Banking - sign up for free here to learn more about our decks.

Join beehiiv: Looking to start your own newsletter? Join beehiiv through us and you’ll get 30 days free and 3 months of a 20% discount.

Join our Referral Program and Gain WSR Investing Club Access ☕️

Enjoyed the newsletter? Send it to a friend 🤝

Obviously, none of this constitutes financial or investment advice. *Today’s piece is in paid partnership with Polymarket