- The Wall Street Rollup

- Posts

- What you Need to Know for April 15th

Welcome back!

And just like that the Iran selloff is over. We’re far from actually “over” though, with Pakistan working to arrange a 2nd round of U.S. and Iran negotiations after last weekend’s talks went nowhere. The blockade of the Strait of Hormuz went into effect on Monday morning.

For now, it seems like the “negotiate/take hard stances over the weekend” positioning is probably we’re heading for yet another weekend. The Banks reported solid numbers to kick off earnings season, so it seems like broadly the U.S. economy is quite fine.

Let’s get into it.

Here’s a look at the earnings still to come this week:

Wednesday: ASML, Morgan Stanley, Bank of America, Progressive, PNC Financial Services, J.B. Hunt

Thursday: Taiwan Semiconductor, Netflix, Pepsico, Abbott Laboratories, Charles Schwab, Prologis, Bank of New York Mellon, U.S. Bancorp

Friday: Truist Financial, Fifth Third Bancorp, State Street, Regions Financial, Ally Financial

Here’s a look at economic data set to be released this week:

Wednesday: Import price index (2.4%), Import price index minus fuel, Empire State manufacturing survey, Home builder confidence index (37), Fed Beige Book

Thursday: Initial jobless claims (215,000), Philadelphia Fed manufacturing survey (12.4), Industrial production (-0.1%), Capacity utilization (76.3%)

Earnings Corner 💸

Goldman Sachs $GS ( ▲ 9.0% ) Beat on both revenue ($17.23B vs. $16.97B) and EPS ($17.55 vs. $16.49) Revenue strength was driven by record equities trading and a rebound in investment banking. The company collected more advisory fees as higher market volatility drove increased client activity and dealmaking. EPS benefited from strong revenue but results were partially offset by weakness in fixed income trading and higher credit provisions. Trading and deal activity remain strong in volatile markets, but some underlying softness and rising credit costs weighed on sentiment. Management struck a more cautious tone, noting geopolitical uncertainty could weigh on dealmaking and market activity.

JPMorgan Chase $JPM ( ▲ 2.5% ) reported a beat on both revenue ($50.5B vs. $49.2B) and EPS ($5.94 vs. $5.45). Results were driven by strong trading and investment banking activity, with fixed income trading rising on elevated market volatility that boosted client activity, alongside a rebound in dealmaking lifting fees. Lower then expected credit costs also helped support earnings, signaling consumers and businesses remain relatively healthy. The bank slightly lowered net interest income outlook, pointing to some pressure from lower rates. Management flagged a more uncertain macro backdrop, citing rising geopolitical and economic risks as well

Citibank $C ( ▼ 5.29% ) Top and bottom line beat with revenue at $24.63B vs. $23.55B and EPS $3.06 vs. $2.65. Revenue reached its highest level in a decade, driven by strong fixed income and equities trading amid elevated volatility, alongside growth in services and banking. EPS was supported by the top line strength. The bank also pointed to continued progress on its restructuring and divestitures. Management also maintained its outlook but flagged macro and geopolitical uncertainty as a potential headwind.

BlackRock $BLK ( ▼ 0.59% ) Beat on both lines with revenue at $6.7B vs. $6.43B and EPS $12.53 vs. $11.5. Results were driven by strong net inflows ($130B), led by record iShares ETF demand alongside continued growth in private markets and technology services. The firm also benefited from higher markets and recent acquisitions (HPS & Preqin), supporting fee growth and margins, with AUM reaching $13.9T. Management highlighted strong momentum and long term growth targets but flagged ongoing macro and geopolitical uncertainty.

Johnson & Johnson $JNJ ( ▼ 1.52% ) Beat on revenue at $24.1B vs. $23.6B and EPS $2.70 vs. $2.66. Results were driven by strong growth in oncology and immunology, with drugs like Darzalex and Tremfya more than offsetting a sharp 60% decline in Stelara due to biosimilar competition. MedTech also remained solid, supporting broader growth across the portfolio. The company raised full year guidance, signaling confidence in continued momentum despite pricing and competitive pressures.

Wells Fargo $WFC ( ▼ 2.72% ) Missed on revenue ($21.4B vs. $21.8B) but beat on EPS ($1.60 vs. $1.58). Results were pressured by weaker net interest income, as higher rates and rising consumer costs weighed on lending profitability, though loan growth remained strong with the loan book surpassing $1T. Management flagged rising energy prices as a potential headwind to consumer spending going forward.

On The Move 📈 📉

Bloom Energy $BE ( ▲ 4.24% ) soared after Oracle announced that its purchasing another $400mm in stock and expanding its capacity partnership with the fuel cell maker.

United Airlines $UAL ( ▼ 0.67% ) and American Airlines $AAL ( ▼ 3.92% ) jumped following rumors Monday evening of a floated merger.

JetBlue Airways $JBLU ( ▼ 4.82% ) rose on raised guidance and talk of potential sale to a larger carrier like United or Southwest.

Meta $META ( ▲ 0.66% ) climbed after extending its deal with Broadcom for custom AI accelerators to 2029, with a commitment to deploy over 1 GW of computing capacity.

AST SpaceMobile $ASTS ( ▲ 1.84% ) fell after Amazon announced its acquisition of Globalstar, adding competition for AST in the direct-to-device satellite connectivity industry.

Adobe $ADBE ( ▼ 4.26% ) and Figma $FIG ( ▲ 0.89% ) were down on Claude set to release an AI design tool

IPO Roundup 📍

Crypto exchange Kraken has filed for a U.S. IPO after freezing its IPO plans last month following Bitcoin’s early-year selloff. Kraken is targeting a $13.3B valuation, vs. $20B last November.

SumUp, a fintech company that makes point-of-sale terminals, is lining up investment banks for a London IPO. The company could be valued at over $10B.

For deeper, stock market research upgrade to the WSR Investing Club

Together With THE AI Excel Superhuman Agent

The Shortcut team just shipped their biggest update yet. Shortcut v0.8 is live with major new releases, including voice mode so you can talk to your spreadsheets like its your Analyst.

The product continues to set new usage records every week, and it's just getting started.

Shortcut is changing how spreadsheet work gets done. So what would it take to make them 10-100x more powerful? The Shortcut team is opening up a research preview for a product they're calling ShortcutXL.

If you want to test on experimental versions with powerful new capabilities, then try out Shortcut and reach out to the team!

Today’s Headlines 📖🍿

March PPI Rundown: Wholesale prices rose 0.5% in March, much lower than expectations of 1.1%, but with an 8.5% jump in energy costs driving the increase. The index grew 4% on an annual basis, marking the largest 12-month gain since February 2023.

Private Credit is still happily on Bank balance sheets: Banks reported over $100B of exposure to private credit firms this earnings season, with JPMorgan at $50B, Wells Fargo at $36B, and Citi at $22B. Dimon added that he’s “not particularly worried” about JPMorgan’s exposure, for losses would have to be very large before banks are hit.

26North raises $6B debut buyout fund: Josh Harris’ 26North Partners closed nearly $6B for its first private equity fund, significantly topping its $4B target, with capital already deployed across seven deals.

TCW Group has marked down its equity stake in Red Lobster by 98% since acquiring the restaurant via its bankruptcy in 2024, with its stake is now worth only $762k after previously being valued at $31mm. TCW still holds $56mm in Red Lobster debt that remains at par, suggesting the terminal value is higher than the total debt.

Cumming Group is up for sale by New Mountain Capital, and Leonard Green is in talks to buy the construction consultancy firm at a $3B valuation. The potential deal comes as PE dealmaking lags behind a wider boom in M&A, with the number for PE-backed deals hitting a six-year low in Q1.

Private credit concerns are overblown according to Franklin Templeton CEO Jenny Johnson, who says that heavily-scrutinized enterprise software companies will be able to repay their borrowings. Johnson adds that it will take decades, not years, for AI to supplant these companies and that the firm’s $100B private credit portfolio has yet to see an increase in delinquencies.

Thoma Bravo winds down growth equity to refocus on buyouts: The $183B software-focused firm is winding down its minority growth strategy launched in 2021, opting to concentrate on controlling buyouts as AI disruption pressures its software portfolio.

Man charged in attack on Sam Altman’s home: A suspect accused of throwing a Molotov cocktail at OpenAI CEO Sam Altman’s residence has been charged with attempted murder, with prosecutors saying he was motivated by anti-AI extremism and carried documents naming additional AI executives and investors.

Meta builds an AI “CEO agent”: Mark Zuckerberg is developing a personal AI agent to retrieve information and shed management layers as Meta pushes companywide AI adoption, flattens teams, and ties AI usage to performance reviews.

Private jet company Bond is expanding its commitment with Bombardier to $5B. The KKR-backed company targets travelers with a net worth of over $500mm for its premium club-like experience in the sky.

Goldman and Ardian bought CIC’s $1B U.S. PE stake, with both firms acquiring the stakes at healthy discounts as China’s sovereign wealth fund sought to reduce its exposure to private markets.

M&A Transactions💭

Acea Energia, provider of energy services, was acquired for EUR 600.0M by Eni Plenitude. Rothschild & Co advised on the sale.

Rana Gruber (OSL: RANA), a sustainable iron ore producer, was acquired for $300.0M by Champion Iron (ASX: CIA). EV/EBITDA was 4.73x and EV/Revenue was 1.99x. Carnegie Investment Bank and DNB Markets Norway advised on the sale.

Waygate Technologies Robotics, provider of non-destructive testing equipment and inspection services, has reached a definitive agreement to be acquired for $1.45B by Hexagon (STO: HEXA B). EV/Revenue was 2.3x. J.P. Morgan advised on the sale.

Secure Energy Services (TSE: SES), operates in waste management and energy infrastructure business, has reached a definitive agreement to be acquired for CAD 6.394B by GFL Environmental (NYS: GFL). EV/EBITDA was 15.7x and EV/Revenue was 4.39x. ATB Capital Markets, Moelis & Company, and RBC Capital Markets advised on the sale.

Leggett & Platt (NYS: LEG), designs and produces engineered components, has reached a definitive agreement to be acquired for $4.156B by Somnigroup International (NYS: SGI). EV/EBITDA was 8.69x and EV/Revenue was 1.02x. J.P. Morgan advised on the sale.

Enjoy Punta Del Este, operator of a hotel and casino, has reached a definitive agreement to be acquired for $160.0M by JHSF Participacoes (BVMF: JHSF3).

Avanos Medical (NYS: AVNS), a medical technology company, has entered into a definitive agreement to be acquired for $1.29B by American Industrial Partners. EV/Revenue was 1.84x. J.P. Morgan and UBS Group advised on the sale.

Globalstar (NAS: GSAT), a telecommunications company, has reached a definitive agreement to be acquired for $11.57B by Amazon.com (NAS: AMZN). EV/EBITDA was 92.16x and EV/Revenue was 42.38x.

Foran Mining, engaged in the acquisition, exploration, and development of mineral properties, was acquired for CAD 4.231B by Eldorado Gold (TSE: ELD). Morgan Stanley, Stifel Financial, and National Bank Capital Markets advised on the sale.

For The Record, developer of digital recording software, was acquired for $212.5M by Tyler Technologies (NYS: TYL). Piper Sandler advised on the sale.

SayanskhimPlast, operator of an organochlorine production complex, was acquired for RUB 30.33B by Rosneft (MISX: ROSN). EV/Net Income was 28.63x and EV/Revenue was 1.43x.

Eurofins MET Labs, provider of laboratory testing and certification services, has reached a definitive agreement to be acquired for EUR 575.0M by UL Solutions (NYS: ULS).

TPG agrees to acquire Learfield, provider of collegiate marketing services, in a deal worth roughly $2.0B.

Galera Therapeutics (PINX: GRTX), a biopharmaceutical company, was acquired through a reverse merger by Obsidian Therapeutics in an all stock deal. Concurrently a $350.0M private placement was completed. The combined company will operate as Obsidian Therapeutics and will be traded on Nasdaq under the ticker symbol “OBX”.

Private Placement Transactions💭

AGS Airports, operator of a network of regional airports, received GBP 350.0M of financing from undisclosed investors.

Slate Auto, manufacturer of a customizable electric vehicle, raised $650.0M of Series C venture funding led by TWG Global.

Rakuten Medical, developer of precision-targeted cancer therapies, raised $111.52M of Series F venture funding led by TaiAx Capital LP.

Neomorph, operator of a biotechnology company, raised $100.0M of Series B venture funding led by Deerfield Management.

Ratio, developer of financial software, raised $115.8M of venture funding through a combination of equity and debt from undisclosed investors.

Shengshu Technology, developer of an AI 3D image generator, raised CNY 2.0B of Series B Venture funding led by Alibaba Cloud Computing at a pre-money valuation of CNY 10.0B.

Want to get the most out of ChatGPT?

ChatGPT is a superpower if you know how to use it correctly.

Discover how HubSpot's guide to AI can elevate both your productivity and creativity to get more things done.

Learn to automate tasks, enhance decision-making, and foster innovation with the power of AI.

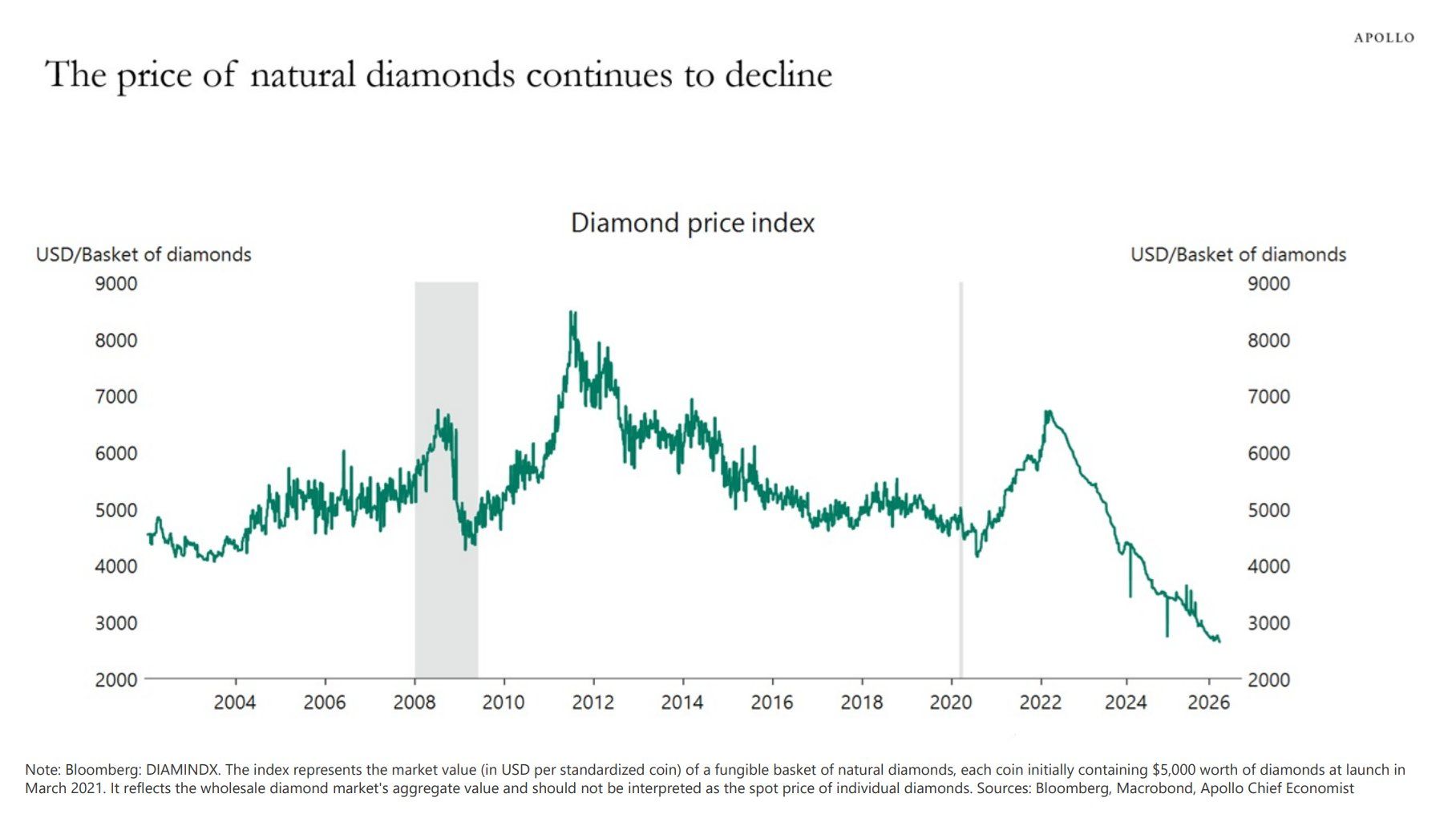

Noteworthy Chart 🧭

Diamond Prices are continuing to crash

Housekeeping Items:

Our Weekly Poll:

How are we doing?Tell us how we're doing and any feedback you have |

Finance Jobs: Looking for a job in Finance? Join Buyside Hub to access the Job Board for free.

Recruit for Investment Banking: High Yield Harry and a group of Investment Bankers put together a 248 page deck for those recruiting for Investment Banking - sign up for free here to learn more about our decks.

Join beehiiv: Looking to start your own newsletter? Join beehiiv through us and you’ll get 30 days free and 3 months of a 20% discount.

Join our Referral Program and Gain WSR Investing Club Access ☕️

Enjoyed the newsletter? Send it to a friend 🤝

Obviously, none of this constitutes financial or investment advice. *Today’s Odds of the Day is in paid partnership with Polymarket