- The Wall Street Rollup

- Posts

- March 29th - The Week Ahead

March 29th - The Week Ahead

Apollo is heading south. "Destruction" is delayed.

HY Harry

March 29, 2026

The Week Ahead Of Us 🔍

Welcome back!

The S&P was down -1.7% on Friday as increased investor worries about the U.S. and Iran War materialized. This was the worst week in the market since the conflict began. Futures are down a touch currently, with the S&P down -0.6% and Nasdaq off -0.75%. Bitcoin’s relief rally has stalled out, with the crypto now hovering around $66k. Meanwhile, the 10-year is up to 4.4%.

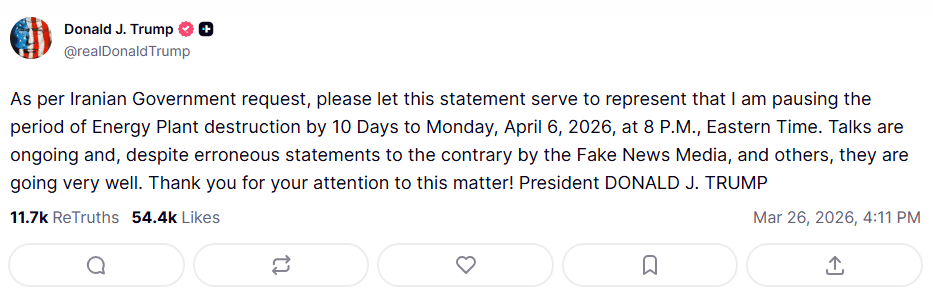

President Trump last week delayed the “period of Energy Plant destruction” to Monday April 6th following ongoing negotiations with Iran. Meanwhile, Pakistan has expressed confidence in the ability to facilitate peace talks between the U.S. and Iran, but it’s unclear if this is formalized yet. Marco Rubio has expressed that he expects the Iran war to be finished in the next couple of weeks. However, the administration is reportedly planning for a boots on the ground deployment of several thousand troops. The Houthis have entered the war, and Israel has been carrying out strikes in Tehran today.

With Trump’s deadline and Rubio’s statements, the U.S. is trying to position sentiment towards the war ending soon, but that doesn’t seem to be indicative of what is happening currently. Remain cautious, even with the possibility of a strong market rally should Trump de-escalate.

Here’s a look at earnings this week.

Tuesday: Nike, McCormick, TD Synnex, Dave & Buster's, FactSet, Beyond Meat, PVH Corp

Wednesday: Conagra Brands, Lamb Weston, MSC Industrial Direct, Tilray Brands

Here’s a look at economic data this week (estimates are in quotations).

Tuesday: S&P Case-Shiller home price index 20 cities, Chicago Business Barometer PMI, Job openings (7.0M), Consumer confidence (88.0)

Wednesday: U.S. retail sales (0.4%), Retail sales minus autos (0.3%), ADP jobs, S&P final U.S. manufacturing PMI, ISM manufacturing (52.0%), Business inventories

Thursday: Initial jobless claims (210,000), U.S. trade deficit (-$61.7 billion)

Friday: U.S. employment report (45,000), U.S. unemployment rate (4.5%), U.S. hourly wages (0.3%), Hourly wages year over year (3.8%), S&P final U.S. services PMI

BDCs in the Age of the ‘SaaS-pocalypse’

Software exposure has become the defining fault line of this BDC earnings season — and if you're assessing private credit portfolios, this briefing is worth your time.

9fin, the leading AI-powered financial intelligence platform covering leveraged finance and private credit, is hosting a live briefing on Tuesday, March 31, at 11 AM ET to unpack Q4 BDC performance and how investors should be positioning amid AI-driven disruption and public market volatility. The discussion will be anchored by 9fin's proprietary BDC dataset — covering non-accrual tracking, NAV and share price monitoring, and software exposure analysis across the public BDC universe.

On the agenda: NAV durability and income resilience; software exposure and underwriting discipline; discounts to NAV and what sentiment is signaling; and the evolving shape of the BDC market in 2026.

Earnings Corner 💸

$CCL ( ▲ 2.14% ) Carnival beat on revenue of $6.17B vs. $6.14B and EPS of $0.20 vs. $0.18, driven by strong bookings, higher ticket pricing, and record onboard spending, with customer deposits reaching nearly $8B. The company cut full year EPS outlook to $2.21 from $2.48 as a sharp rise in fuel costs tied to geopolitical tensions is expected to add $500M in expenses, pressuring margins despite strong demand. Shares fell following the update.

On The Move 📈 📉

Cyber stocks traded off Friday following an internal memo from Claude leaked that revealed “Mythos”, a new model that may cause “unprecedented cybersecurity risks” stocks like $OKTA ( ▲ 4.21% ) $S ( ▲ 6.35% ) and $CRWD ( ▲ 3.31% ) were all hit

Unity Software $U ( ▲ 5.69% ) stock surged after issuing stronger-than-expected Q1 guidance, projecting revenue of $480M-$505M and higher adjusted EBITDA. Shares remain down 55% YTD despite the rebound.

Figma $FIG ( ▲ 10.57% ) stock declined as Google positions itself as a competitor within the design software space.

Airbnb $ABNB ( ▲ 2.59% ) shares fell as oil prices and TSA staffing disruptions weighed on travel sentiment.

Starbucks $SBUX ( ▲ 1.4% ) shares slipped as investors negatively assessed operational changes, including kiosk formats and a renewed emphasis on sit-down experiences.

IPO Roundup 📍

Anthropic is considering an IPO as soon as October, with Goldman Sachs, JPMorgan, and Morgan Stanley in early talks for lead roles. The company was valued at $380B in a recent funding round and seeks to raise $60B+.

PE-backed convenience store operator Yesway filed for a US IPO, targeting a potential $300M raise. The company posted $2.7B in revenue in 2025.

Babylist, a baby registry platform, is weighing a potential 2027 IPO after revenue jumped 45% in 2025 to $750M+. The company is targeting $1B in 2026 sales.

For deeper, stock market research upgrade to the WSR Investing Club

Today’s Headlines 📖🍿

OpenAI-Anthropic feud shapes the future of AI: A decade-long power struggle between Sam Altman and Dario Amodei is spilling into public view, with disagreements over AI safety, government contracts, and leadership philosophy defining the rivalry between the two firms as they both race toward potential IPOs.

Mortgage rates rise, consumer confidence: 30-year mortgage rates have surged to 6.38%, a tough setup going into spring selling season, especially compared to the <6% rates we were flirting with just a month ago. Meanwhile, consumer confidence in March fell from 56.6 to 53.3 (est. of 54) due to worries over the Iran war and rising gas prices.

Microsoft takes over AI data center capacity, renting about 900MW in Texas that was previously planned for Oracle and OpenAI, highlighting continued demand for AI infrastructure even when one party steps out.

Meanwhile, SoftBank secured a record $40B bridge loan to fund its growing stake in OpenAI.

Permira targets discounted European software debt, after AI disruption fears sparked a selloff, arguing markets have overreacted. Permira’s head of strategic opportunities said “A lot of these names, we just don’t believe will go through restructuring.”

BofA, Citi, and Apollo move to offload $57.5B in Warner Bros LBO Debt, with syndication potentially wrapping up at the end of this week.

Apollo is planning a move down south: The asset management giant is set to establish a 2nd HQ in either south Florida or Texas, according to a statement written to the FT.

Asia PE funds saw the lowest fundraising environment in a year, according to Bain, with just $58B in fundraising closed, compared to 2021’s peak of $180B. Asia’s share of global fundraising fell to 5%.

Blackstone and industrial investor Tinicum are among the bidders to acquire UK aerospace parts supplier Senior, with shares trading around £2.77, the company is valued at ~£1.16B today. Advent and Arcline are also involved, and Advent’s £2.72 a share bid was previously rejected.

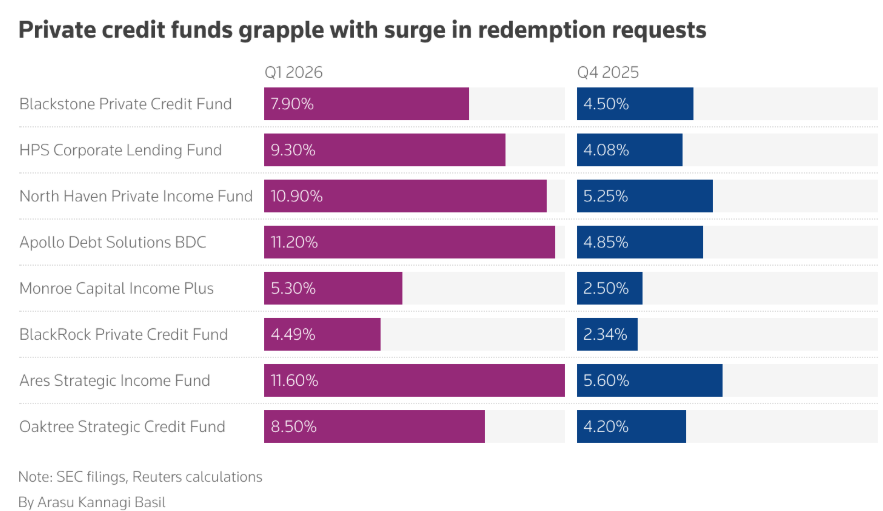

An Oaktree private credit fund met 8.5% withdrawal requests, honoring the full request vs. the usual 5% quarterly cap. Here’s a great chart below on how redemptions have hit private credit managers so far:

TSA Agents will be paid during the shutdown following an executive order from President Trump.

PlayStation prices are on the rise, with the PS5 console rising from $549.99 to $649.99 effective April 2nd.

Expect no reprieve here - with chip costs on the rise due to AI demand, gamers are left with higher prices as a result.

Netflix is raising U.S. prices: Standard with Ads Plans are getting raised by $1 to $8.99, while Standard without Ads and Premium plans are getting raised by $2 each to $19.99/month and $26.99/month, respectively.

M&A Transactions💭

Olaplex Holdings (NAS: OLPX), a beauty company, has reached a definitive agreement to be acquired for $1.848B by Henkel (ETR: HEN3). EV/EBITDA was 24.89x and EV/Revenue was 4.37x. J.P. Morgan advised on the sale.

Dolly Varden Silver (TSX: DV), a mineral exploration company, was acquired for $812.003M by Contango ORE (ASE: CTGO). Haywood Securities and Raymond James advised on the sale.

Bioniq, producer of personalized nutritional supplements, has reached a definitive agreement to be acquired for $150.0M by Herbalife Nutrition (NYS: HLF).

Motorola Solutions Canada Network has reached a definitive agreement to acquire The Land Mobile Radio Networks Services Business of Bell Canada for CAD 675.0M.

ATM Gaming, developer of party board games, has reached a definitive agreement to be acquired for EUR 180.0M Asmodee (STO: ASMDEE B).

Xanadu, developer of photonic quantum computing hardware, was acquired for $500.0M by Crane Harbor Acquisition through a reverse merger. The company also received $275.0M of development capital from Georgian, MMCAP International, and Planet First Partners.

Transcend Therapeutics, operator of a neuroscience focused clinical stage company, has reached a definitive agreement to be acquired for JPY 111.6B by Otsuka Pharmaceutical.

Ravelin Properties (TSE: RPR.UN), an unincorporated, open-ended real estate investment trust, has entered into a definitive agreement to be acquired for $1.1B by Clarke. EV/Revenue was 9.86x. KSV Advisory advised on the sale.

Pension Insurance Corporation, provider of insurance services, was acquired for GBP 5.7B by Athora.

Excellergy, developer of protein therapeutics, has reached a definitive agreement to be acquired for $2.0B by Novartis (SWX: NOVN). J.P. Morgan advised on the sale.

Private Placement Transactions💭

Wefox, developer of a comparison platform, raised EUR 166.0M of venture funding through a combination of debt and equity. EUR 91.0M was raised from Chrysalis Investments and SBI Investment.

Shield AI, operator of a defense technology company, raised $2.0B of Series G venture funding led by The Resilience Initiative, Advent International, and JP Morgan Chase at a pre-money valuation of $11.0B.

Nordic Knots, manufacturer of home furnishing products, raised an estimated $100.0M of venture funding in a deal led by Imaginary Ventures.

eMed, developer of a clinician-led GLP-1 care program, raised $200.0M of Series A venture funding led by Aon.

Cents, developer of laundromat management software, raised $140.0M of Series C venture funding led by Sumeru Equity Partners.

AIONX, developer of a hyperscale data center, raised EUR 100.0M of venture funding through a combination of convertible debt and equity from Stoneweg Europe Stapled.

Polymarket, operator of an information market platform, raised $2.6B of Series D venture funding through a combination of debt and equity from Electric Feel Ventures, Intercontinental Exchange, and Dubin & Co. at a pre-money valuation of $8.0B.

Odds of the Day 🍒

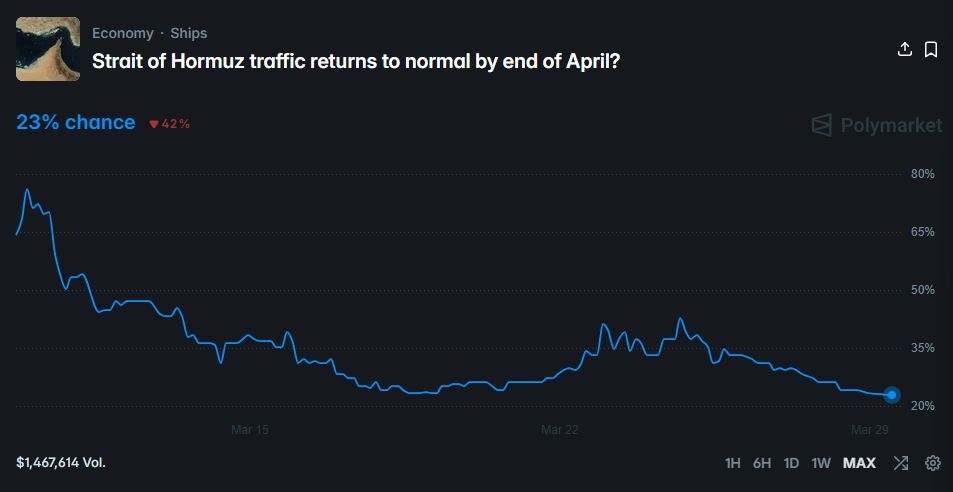

Polymarket traders are pricing in only a 23% chance of Strait of Hormuz traffic returning to normal by the end of April.

Experts Would Invest $100,000 in This Alternative Now

A new report shows 44% of family offices are investing more in residential real estate. Now, you can access these assets with mogul. This platform lets you invest in properties producing +7% yields and 18% IRRs. Plus, they do all the property management for you.

Past performance isn't predictive; illustrative only. Investing risks principal; no securities offer. See important Disclaimers

Noteworthy Chart 🧭

Housekeeping Items:

Our Weekly Poll:

How are we doing?Tell us how we're doing and any feedback you have |

Join our Referral Program and Gain WSR Investing Club Access ☕️

Enjoyed the newsletter? Send it to a friend 🤝

Obviously, none of this constitutes financial or investment advice. Today’s piece is sponsored by 9fin. *Today’s Odds of the Day is in paid partnership with Polymarket