- The Wall Street Rollup

- Posts

- April 5th - The Week Ahead

April 5th - The Week Ahead

Iran's Deadline is almost here. More OpenAI infighting.

HY Harry

April 05, 2026

The Week Ahead Of Us 🔍

Welcome back!

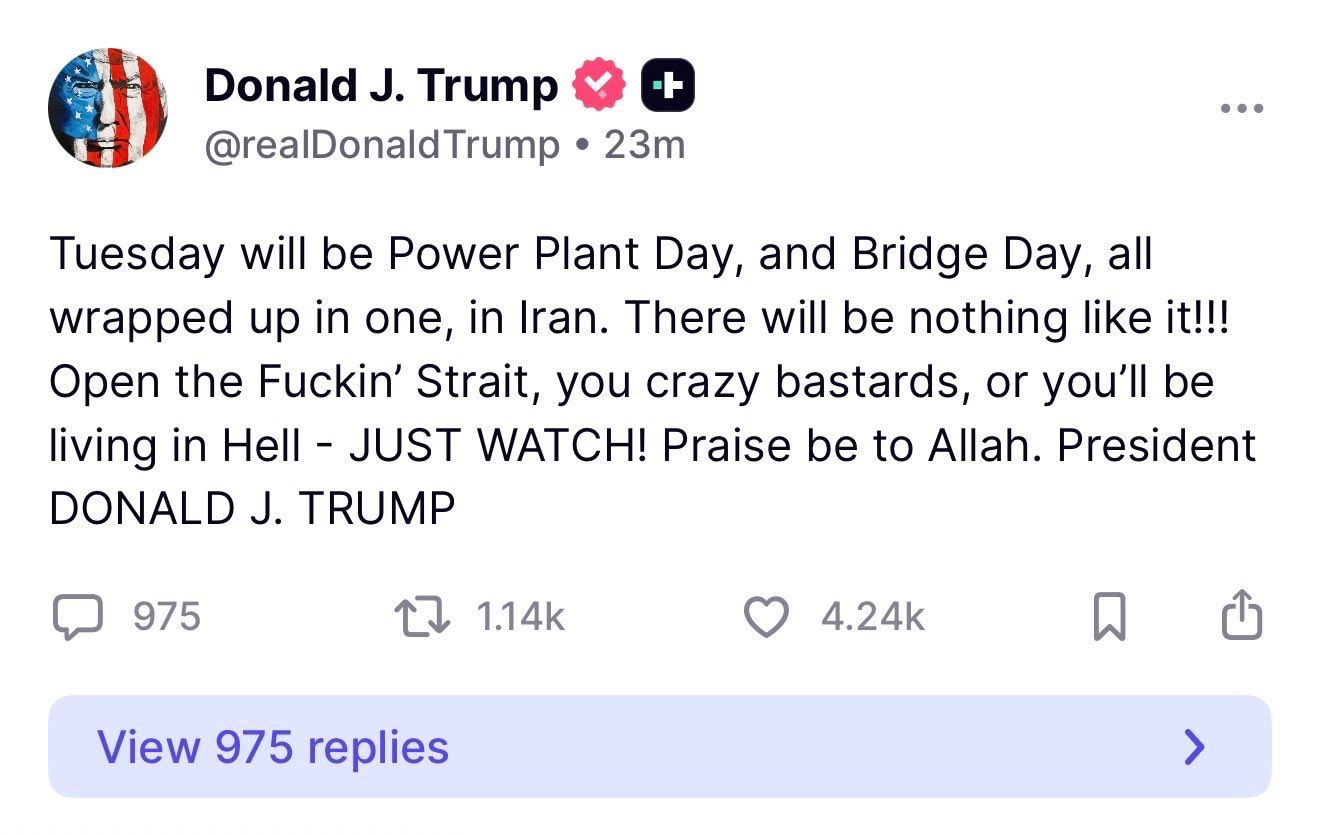

After an abbreviated trading week, we have the S&P and Nasdaq down -0.6% and -0.6% respectively following Trump’s warning that a deal must be reached by Tuesday at 8pm ET. If not, Trump will strike “every power plant and every bridge” in Iran. Crude has now shot up to $113/barrel. I have to fill up my car tomorrow and am not looking forward to it! Trump still believes he can get a deal done with Iran in advance of Tuesday, but he is also set to have a news conference with the US Military at 1pm tomorrow.

According to Iran, 15 ships have passed through the Strait of Hormuz over the past 24 hours (compares to the usual 138 ships per day). Bizarrely, Citrini has sent one of their Analysts to the Strait of Hormuz to do boots on the ground channel checks.

A lot of our Sunday night posts have been quickly met with “Wait, here’s another pause or delay!”….so let’s see what happens this week…

We put a new WSR IC piece on IEH Corporation last week. Our 40% off offer expires in 3 days - so take action now.

As a reminder, we are moving to 3x/week (outside of Holidays) so expect seeing us on Wednesday and Friday mornings. Let’s get into it.

This Week’s Calendar:

Here’s a look at earnings this week.

Tuesday: Levi Strauss

Wednesday: Delta Air Lines, Constellation Brands, RPM International, Applied Digital

Thursday: WD-40, BlackBerry Limited, Simply Good Foods

Here’s a look at economic data this week (estimates are in quotations).

Monday: ISM Services (55.4%)

Tuesday: Durable goods orders (-1.0%), Durable-goods minus transportation, Consumer credit ($10.0B)

Wednesday: Fed Meeting Minutes

Thursday: Personal income (0.3%), Personal spending (0.5%), PCE index (0.4%), PCE y/y (2.8%), Core PCE index (0.4%), Core PCE y/y (3.0%), GDP second revision (0.7%), Initial jobless claims (210,000), Wholesale inventories (-0.5%)

Friday: Consumer price index (1.0%), CPI y/y (3.3%), Core CPI (0.3%) Core CPI y/y (2.7%), Factory orders (0.2%), Consumer sentiment prelim (52.0)

A Message from Polymarket: What Smart Money Knows

Polymarket is the world's largest prediction market, with a 90%+ accurate track record on interest rates, corporate earnings, and geopolitical risks.

When you read The Oracle by Polymarket, you'll learn to think like the top 0.1% of forecasters on Polymarket; traders who stop at nothing to develop unique insights on the news.

The Oracle takes you inside their unusual playbooks.

What's Inside:

🔮 TILTED: How 'Betwick' lost 70% of his bankroll and climbed Back to $800k

Read it here

On The Move 📈 📉

$SBAC ( ▲ 2.11% ) SBA Communications Corporation shares surged after reports the company is exploring a potential sale following takeover interest from infrastructure funds.

Space stocks have been on the move higher, with $YSS ( ▲ 1.26% ) $VSAT ( ▲ 0.05% ) $PL ( ▼ 0.73% ) $TSAT ( ▼ 1.39% ) and $IRDM ( ▼ 3.54% ) among those moving higher on SpaceX’s IPO filing, momentum from recent NASA milestones, and broader optimism around falling launch costs and expanding space infrastructure demand.

$WIX ( ▲ 0.96% ) Wix.com shares fell after analysts downgraded the stock as the company’s core business is expected to slow (12% growth to 8% growth), while higher AI and marketing spending is set to pressure margins and reduce profitability.

$TSLA ( ▼ 7.49% ) Tesla shares fell after reporting weaker-than-expected Q1 deliveries of ~358K vehicles, missing estimates and signaling soft demand as production outpaced deliveries, leading to rising inventory.

IPO Roundup 📍

SpaceX is now targeting a valuation above $2T in its IPO and could raise as much as $75B, potentially marking the largest listing ever. The company has begun floating the valuation to investors as it lines up anchor backers, with banks such as Bank of America, Citigroup, Goldman Sachs, and a broader syndicate of up to 21 banks.

Barrick Mining has hired Goldman to lead the IPO of its gold assets in a deal that could give the new company a valuation of more than $60B.

For deeper, stock market research upgrade to the WSR Investing Club

We just put out a great new piece on IEH Corporation

Today’s Headlines 📖🍿

U.S. job growth in March was +178k, well above estimates of +70k. Unemployment was lower m/m to 4.3%, but that was due to lower labor force participation. However, February jobs have been revised to a 133k loss, down from an initially reported 92k loss.

The real story - Healthcare is carrying the job market. Over the past 12 months, the healthcare industry has added 663k jobs while most other sectors have contracted over the same period.

Altman and OpenAI’s CFO are diverging on IPO timing: Altman and CFO Sarah Friar are apparently in disagreement re: timing of an IPO. Altman is rushing towards an IPO, while Friar is worried about revenue growth and compute spend. As a result, she has been left out of financial planning meetings by Altman, and began reporting to the head of applications instead of Altman.

Meanwhile, OpenAI is reshuffling leadership: Longtime COO Brad Lightcap is now set to lead special projects and will oversee OpenAI’s push to sell its software to businesses through joint ventures with PE firms. Additionally, CMO Kate Rouch and AGI development CEO Fidji Simo are stepping away for medical reasons.

Blue Owl limits redemptions: The firm enforced its 5% withdrawal limit after investors in the Blue Owl Credit Income Corp. and Blue Owl Technology Income Corp. asked to pull 22% and 41% of shares, respectively. Blue Owl had previously met redemption requests above the 5% level for these funds.

KKR raises $23B for North America PE fund: The firm closed its largest-ever North America-focused private equity vehicle, underscoring sustained LP appetite for private markets. KKR’s PE AUM now stands at ~$229B.

Ares leads a private credit CV: Ares was the lead investor in a $1.7B continuation vehicle of more than 200 1L loans originated and managed by Antares. Generally, continuation vehicles for private credit are atypical, but this marked the second deal between the firms in the past year.

PE fundraising hits decade low: Buyout firms raised just $86B in Q1, putting 2026 on pace for the weakest annual total since 2016 as private credit stress, software volatility, and the Iran war weigh on LP sentiment.

3 Gulf Funds are backing Paramount’s $81B takeover of Warner Bros: Saudi Arabia’s Public Investment Fund is providing $10B, a big slug of the $23B+ David Ellison is receiving from Middle-East funds to help finance his Warner Bros Discovery takeover.

Caa1-rated Cleaning-products maker PLZ turns to private credit to refinance its ~$1B in BSL market debt, with Ares and Antares arranging the financing for the Pritzker-backed company.

A Maine bill banning new data center construction is expected to pass in the Senate, freezing data-center projects of at least 20 megawatts until November 2027 so the state can assess their impact on the environment and electricity grid.

Maintenance covenants continue to loosen: Nearly half of deals from 2024-2025 set leverage thresholds at 8x EBITDA or higher, while 26% set leverage thresholds at 9x or higher.

Genesis HealthCare Assets are sold, following its bankruptcy: NewGen is officially acquiring 200 nursing homes from Genesis HealthCare, which filed for bankruptcy in last July.

Mercury is in talks to raise at a $5B valuation after hitting $650mm in annualized revenue in 2025. The fintech startup recently acquired Central, a payroll and benefits service, as it expands into small business and personal banking.

Musk ties Grok to SpaceX IPO mandates: Banks vying to advise on SpaceX’s IPO are being required to purchase subscriptions to Musk’s AI chatbot Grok, with some firms committing tens of millions of dollars.

M&A Transactions💭

OpenAI acquires TBPN, a daily, live tech talk show and one of the fastest-growing media companies, for reportedly “low-hundreds of millions of dollars”.

VISUfarma, operator of an ophthalmic specialty pharmaceutical company, has reached a definitive agreement to be acquired for EUR 190.0M by Lupin (BOM: 500257). EV/Revenue was 3.67x. Stifel advised on the sale.

Vibrant Energy, developer of clean renewable energy infrastructure, was acquired for INR 50.0B by Inox Green Energy Services (BOM: 543667). J.P. Morgan advised on the sale.

The Employee Health and Safety Software Business of UL Solutions (NYS: ULS) was acquired for $210.0M by Peak Rock Capital. EV/Revenue was 3.75x. Houlihan Lokey advised on the sale.

The Flexitallic Group, manufacturer of industrial static sealing products, was acquired for $475.1M by Groupe Michelin (PAR: ML). EV/Revenue was 2.16x. Citigroup advised on the sale.

The Container Store, operator of a chain of retail stores, has reached a definitive agreement to be acquired for $150.0M by Bed Bath & Beyond (NYS: BBBY).

S E & M Constructors, operator of a full-service mechanical, electrical, and plumbing contractor service, was acquired for $158.0M by Everus Construction Group (NYS: ECG). EV/Revenue was 1.45x. FMI advised on the sale.

The North Island Operations of Synlait Milk (NZE: SML) were acquired by Abbot (NYS: ABT) for NZD 307.0M.

The Edaravone Business of Mitsubishi Tanabe Pharma was acquired by Shionogi & Co. (TKS: 4507) for $2.5B. Centerview Partners and Goldman Sachs advised on the sale.

Leonardo Hotel London Aldgate was acquired for GBP 130.0M by Leonardo Hotel Management.

Four Roses Distillery, producer of bourbons handcrafted beverage, was acquired for JPY 120.0B by E. & J. Gallo Winery. UBS Group advised on the sale.

160over90, provider of marketing and brand strategy services, has reached a definitive agreement to be acquired for $500.0M by Publicis Groupe (PAR: PUB).

Starbucks China, operator of a chain of coffee restaurants in China, was acquired for $4.0B by Boyu Capital. EV/EBITDA was 14.81x and EV/Revenue was 2.15x. Goldman Sachs advised on the sale.

Coefficient Bio, a company in stealth mode, was acquired for $400.0M by Anthropic.

Private Placement Transactions💭

Vulcan Elements, manufacturer of rare earth magnets, raised $430.72M of venture funding from undisclosed investors.

Galaxea AI, developer and manufacturer of embodied intelligent robots, raised CNY 2.0B of Series B+ venture funding from Lens Technology, Beijing Science and Technology Innovation Fund, and Aviation Development Fund Management at a pre-money valuation of CNY 18.0B.

Newrite Medical, developer of targeted therapeutic and diagnostic agents, raised CNY 1.0B of Series E venture funding led by Shanghai STVC Group, Nanjing Gaoke Xinjun, and Guoxin Capital.

Join our Referral Program and Gain WSR Investing Club Access ☕️

Want to get access to WSR IC without having to pay? Well, just refer the newsletter around to your friends and peers:

Housekeeping Items:

Our Weekly Poll:

How are we doing?Tell us how we're doing and any feedback you have |

Shop our Affiliate Offers: Looking for professional clothing, watches, blue light glasses, desks, keyboards, and chairs? Shop here through our affiliate program to buy the finance professional essentials that you were going to buy anyways through us!

Finance Jobs: Looking for a job in Finance? Join Buyside Hub to access the Job Board for free.

Upgrade to the WSR Investing Club: Wall Street Rollup readers get 40% off for their first 12 months. Receive high-conviction stock research & analysis to help you cut through the noise.

Recruit for Investment Banking: High Yield Harry and a group of Investment Bankers put together a 248 page deck for those recruiting for Investment Banking - sign up for free here to learn more about our decks.

Join beehiiv: Looking to start your own newsletter? Join beehiiv through us and you’ll get 30 days free and 3 months of a 20% discount.

Obviously, none of this constitutes financial or investment advice. *Today’s paid partnership is with Polymarket